Monetary oxymoron

- Gustavo A Cano, CFA, FRM

- Mar 28

- 1 min read

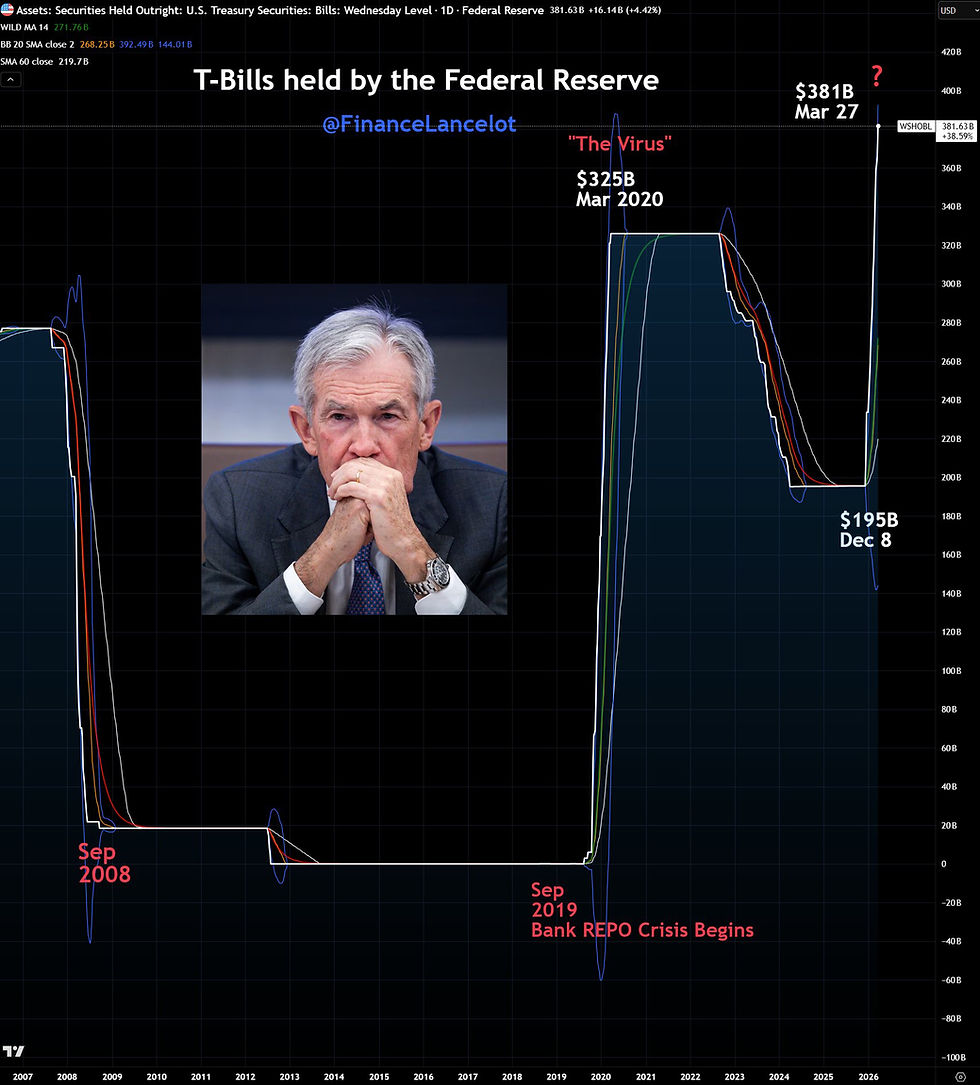

In December 2025, after ending its balance sheet reduction (quantitative tightening) on December 1, the FOMC directed the New York Fed’s Open Market Trading Desk to begin Reserve Management Purchases (RMPs) of Treasury bills. The purpose: Maintain an “ample reserves” regime by offsetting seasonal and trend growth in non-reserve liabilities. This prevents tightness in short-term money markets and ensures effective control over the federal funds rate. It is explicitly not monetary policy easing or quantitative easing (QE) in the traditional sense. In simple terms, it’s not a duck, but it quacks like one, so perhaps it is monetary easing. The Fed started buying $40Bn a month and is now buying $20Bn plus reinvestment of their sales of mortgages that run off. The bottom line: the Fed will be this year the largest net buyer of T-bills in 2026 ( ~$300–400 billion total for the year). At the same time, the Fed has published a paper yesterday titled “A User’s Guide to Reducing the Federal Reserve’s Balance Sheet”. We’re busy chasing missiles in the gulf while the Fed is working on a huge monetary oxymoron where the goal is to reduce the balance sheet from 21% of GDP to 15%, while making sure there is ample liquidity (?). Rate cuts seem to be out of the table for the foreseeable future, and the Fed wants to reduce its balance sheet, in the middle of a potential liquidity crisis in the credit market. What can go wrong?

Want to know more? You can register for free at Fund@mental.

#iamfundamental #soyfundamental #wealthmanagement #familyoffice #financialadvisor #financialplanning #policymistake #ratecut #stagflation

Comments