No clear path

- Gustavo A Cano, CFA, FRM

- Mar 30

- 2 min read

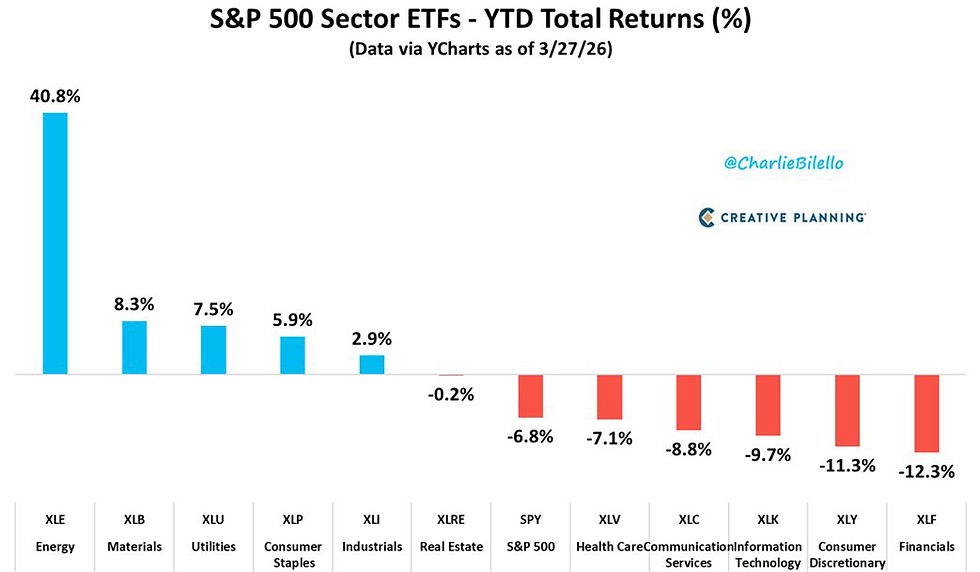

The Nasdaq 100 and the DJIA are in correction territory (-10%) from the maximums. The S&P500 will join them soon. Brent oil, just reached $116 and continues to inflict pain all over the world. The Iranian conflict shock, with the continued closure of the strait of Hormuz has changed the narrative, direction and leadership of the U.S. stock market. In January, it was still a growth story, with mag7, AI and the rapid intervention in Venezuela, at the center of the universe. February brought us worries in Private credit and the software sub sector, on the back of the almighty AI agents. And just when the market was digesting those news, Israel and the US started the armed conflict with Iran. We’re now in its fifth week, and you can see below the YTD performance of the S&P500 sectors: Energy is by far the best one and financials are the worst. Third from the bottom is Tech, with a much needed correction that will allow a future upside leg, once the air clears. For the first time in 10 years, NVDA forward P/E is at par with the S&P500 index. The index is till very much concentrated, but valuations are adjusting. The bond market is the one getting most attention: the 2 year treasury touched 4% (YTM) on Friday, and has since retreated to 3.88%. This is way above current Fed funds, and it flashes danger. It’s whispering there might be a rate hike, and then corrects itself trying to forget that possibility. Markets are still looking for equilibrium, but it cannot find it with an elevated oil price and the geopolitical noise.

Want to know more? You can register for free at Fund@mental.

#iamfundamental #soyfundamental #wealthmanagement #familyoffice #financialadvisor #financialplanning #policymistake #ratecut #stagflation

Comments