The new Sharpe regime

- Gustavo A Cano, CFA, FRM

- Nov 4, 2023

- 1 min read

Modern Portfolio theory puts a lot of emphasis on risk adjusted returns. Investing, accordingly, is not only about obtaining the highest returns, but higher returns assuming the minimum amount of risk, and for that we must use an ex-post measure, volatility. In the chart below, there is a comprehensive list of assets sorted by Sharpe ratio, which measures (excess) returns per unit of volatility over the last 5 years. CTAs are at the top of the list, since they have benefited from the run up in commodities due to inflation. Gold, is aso at the top of the list, signaling that perhaps fiat currencies are losing that trust component due to increasing government debt. But at the bottom of the list, we find the global Agg index and long term bonds. That is quite unusual, and it tells us the market has shifted from a steady decrease in yields since the 80’s to a new upward yield regime, dominated by inflation, that we haven’t seen in decades. If we’re witnessing a reversal to the mean, we’re on for a long trip on upward yields.

Want to know more? join Fund@mental here https://apps.apple.com/us/app/fund-mental/id1495036084

#iamfundamental #soyfundamental #wealthmanagement #familyoffice #financialadvisor #financialplanning

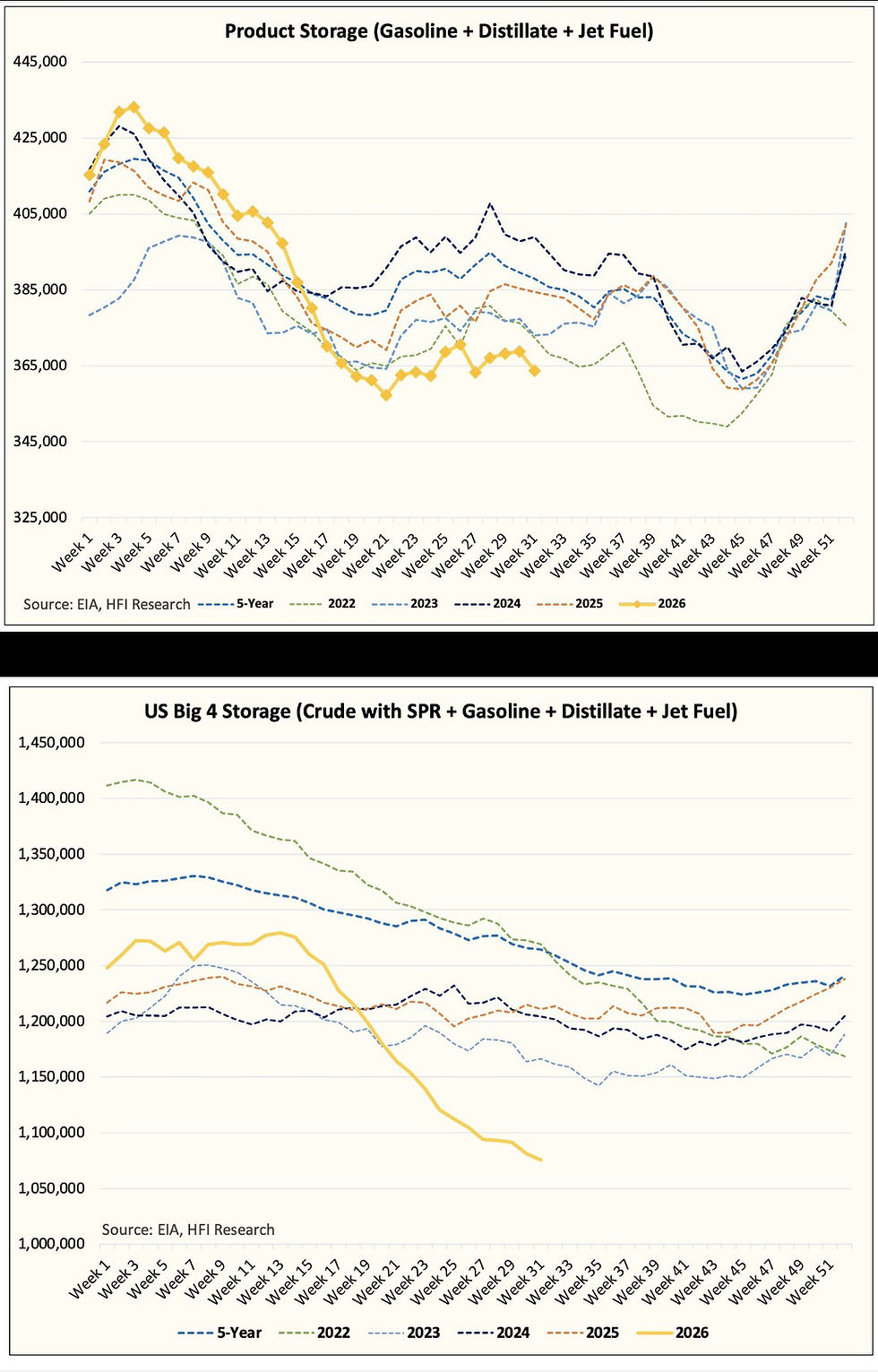

Source: Jurrien Timmer

Comments